REPORT: Toronto’s most and least expensive neighbourhoods for car insurance

We identified 13 postal codes in the City of Toronto with the least and most expensive rates. See how your neighbourhood compares to the city’s average for auto insurance rates.

March 25, 2021

10-minute read

The average cost of car insurance in Toronto continues to rise slowly. LowestRates.ca data show that from 2019 to 2020, motorists in the city were dealt a 3% increase in average premiums, and year-to-date, the average cost of car insurance in Toronto is flat versus 2020, with an increase of just 0.5%.

Looking at that data doesn’t exactly inspire confidence that drivers can secure lower car insurance rates in Toronto than they paid in the past. But depending on what neighbourhood you live in, it’s possible that you could pay less than the city’s average. It's also possible that you could pay more.

Using 2020 data from the LowestRates.ca auto insurance quoter, we break down the most and least expensive neighbourhoods in the City of Toronto for car insurance.

In past reports, we’ve outlined the cost of insurance across the GTA but for the purposes of this report, we’ve decided to go more granular and focus solely on neighbourhoods within the inner City of Toronto.

To do this, we referenced data of drivers between 30 and 39 years of age with clean records who completed car insurance quotes on our site in 2020. So, how do we determine which neighbourhoods are most or least expensive? For this report, we started with what the average price of auto insurance was in Toronto. Then we searched for the neighbourhoods that deviated from that by 10%. So if your neighbourhood is 17% more expensive than the average, it makes the most expensive list. And vice versa.

It’s important to acknowledge that many different factors impact insurance rates in a given area. This can include the number of claims, tickets, driving violations, as well as where drivers can park their vehicles (laneway, street, garage), how congested it is, and whether drivers often speed in the area, and so on. While we can’t definitively state why rates are X in one neighbourhood and Y in another, we can speculate based on factors like these.

Key findings:

- The average cost of car insurance in the city of Toronto has increased by 3.5% (YTD) since 2019.

- The most expensive neighbourhoods for car insurance in Toronto include: Eglinton West, Corso Italia, Forest Hill, Cabbagetown, and Oakwood-Vaughan.

- Neighbourhoods in Toronto with the cheapest car insurance include: Trinity-Bellwoods, Old Mill, Little Italy, Roncesvalles, and Koreatown.

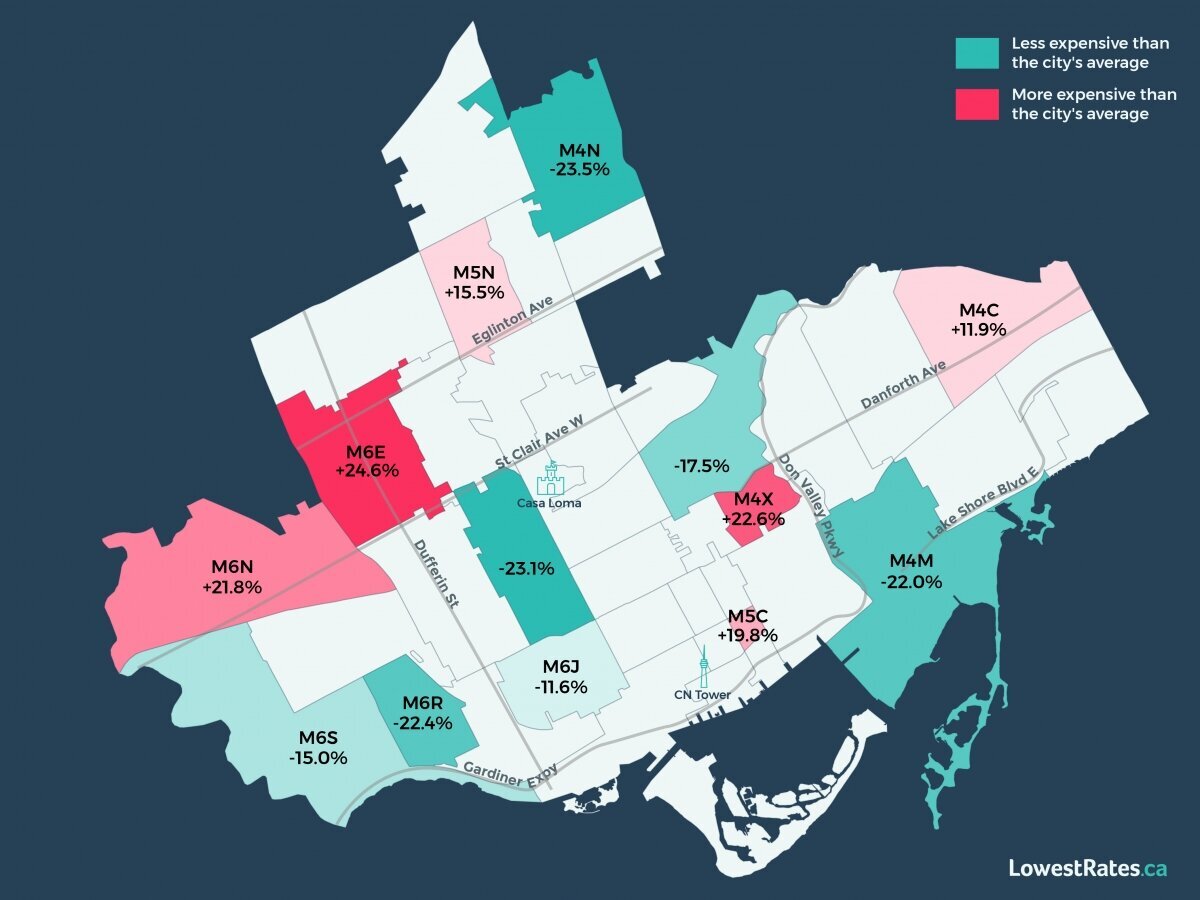

Toronto’s most expensive neighbourhoods for car insurance

1. M6E: 24.6% more expensive than the city’s average

Neighbourhoods within this postal code: Northcliffe Village, Oakwood-Vaughan, Caledonia-Fairbank, Fairbank, Belgravia, St. Clair West Village, Corso Italia, Eglinton West (Little Jamaica), Earlscourt

The M6E postal code encompasses neighbourhoods that are close to Eglinton Avenue, as well as Allen Road and the 401. Close proximity to a major highway, coupled with the fact that much of Eglinton is (still) under construction, means that there’s significant congestion in this area. This could contribute to higher insurance rates, as could the fact that people in this neighbourhood might be driving faster than normal as they get on and off the highway.

Each of these factors can spell higher risk of damage/collisions to insurance companies, and therefore, higher premiums.

2. M4X: 22.6% more expensive than the city’s average

Neighbourhoods within this postal code: St. James Town, Cabbagetown

St. James Town is one of the most densely populated neighbourhoods in North America, which could be contributing to higher car insurance rates. The more people, the more vehicles, the more congestion, and the higher likelihood of claims.

Both St. James Town and Cabbageotwn are also located just west of the Don Valley Parkway, a major highway, and in between Queen and Dundas, which are two busy streetcar routes. There could be lots of one-way streets in this area, as well as mostly street parking — all of which could explain why rates in this postal code are higher than the city’s average.

3. M6N: 21.8% more expensive than the city’s average

Neighbourhoods within this postal code: Rockliffe-Smythe, Mount Dennis, Smythe Park, Stockyards District, Carleton Village, Harwood, Pelham Park, Roselands, Syme

The Stockyards District is home to a major driver-centric shopping centre, which could increase the risk of collisions. As well, Keele Street cuts through many of these neighbourhoods. When looking at insurance rates, it’s important to consider how people are driving in a given area. Keele is a major south-west street that connects drivers to the 401. This means people could be driving faster on it than on other streets, which increases the likelihood of collisions, and therefore results in higher premiums.

There’s also the fact that these neighbourhoods are just on the cusp of the southeast border of Toronto's highest area for vehicle thefts, according to the Toronto Star, which could also be contributing to higher rates.

4. M5C: 19.8% more expensive than the city’s average

Neighbourhoods within this postal code: Downtown Toronto, Old Town Toronto

The M5C postal code includes parts of the downtown financial district. This means narrower streets, more congestion, more underground parking lots (which are ripe for collisions) as well as street parking, which insurance companies see as riskier than being able to park in a laneway or garage.

5. M5N: 15.5% more expensive than the city’s average

Neighbourhoods within this postal code: Caribou Park, Allenby, Lytton Park, Lawrence Park South, Forest Hill

The Forest Hill and surrounding neighbourhoods are situated between Eglinton and Lawrence, which are two major east-west streets that get drivers across the city. There are also a few schools in this area.

Chaplin Crescent also cuts through these neighbourhoods This is a major throughway for drivers looking to cut across the city, which means it’s likely more congested on the regular.

6. M4C: 11.9% more expensive than the city’s average

Neighbourhoods within this postal code: Danforth Village, East Danforth, Woodbine Heights, Woodbine-Lumsden, Crescent Town, Todmorden Village, Old East York

The M4C postal code includes neighbourhoods near the Danforth, which is a busy Toronto street. There’s also easy access to the DVP from this area, which could also account for higher rates, since people getting on and off the DVP are probably driving faster. Speeding on the DVP was certainly an issue during the first lockdown of 2020, as those still on the road were driving much faster due to the extra space they had.

Toronto’s least expensive neighbourhoods for car insurance

7. M6J: 11.6% less expensive than the city’s average

Neighbourhoods within this postal code: Trinity-Bellwoods, West Queen West, Beaconsfield Village

The M6J postal code includes two of the most popular neighbourhoods for young people in Toronto: Trinity-Bellwoods and West Queen West.

Stretching along Queen Street from Bathurst Street to Gladstone Avenue, a majority of the people in this neighbourhood likely do not drive, as there’s a wealth of transit options nearby. It’s likely that most residents of these neighbourhoods primarily bike, walk, or use transit to get around, which could explain the lower car insurance premiums.

8. M6S: 15.0% less expensive than the city’s average

Neighbourhoods within this postal code: Runnymede, Swansea, Bloor West Village, Lambton, Warren Park, Baby Point, Old Mill

The M6S postal code encompasses neighbourhoods in the York-Crosstown region. The major streets in this area are Bloor Street, Jane Street, and Runnymede Road.

The pedestrian-friendly neighbourhoods are fairly easy to get around without a car. Most errands can be accomplished on foot and the area is very bikeable. Residents living in this area likely don’t drive much within the city and can take advantage of the two subway stations in the neighbourhood.

The fewer cars on the road, the less the likelihood of collisions and theft. And since insurance companies calculate premiums based on the level of future risk, the lack of congestion in this area could be translating into cheaper premiums.

9. M4W: 17.5% less expensive than the city’s average

Neighbourhoods within this postal code: Rosedale, Governor's Bridge

Rosedale and Governor’s Bridge are among the most affluent areas in Toronto. It’s not unreasonable to assume that drivers in this area might be better financially positioned to pay out of pocket for damage to their vehicles rather than put in a small claim with their insurance company. It’s also likely that insurance customers in these neighbourhoods pay their insurance premiums on time, all of which can result in less expensive premiums.

Similarly, where you park your vehicle also has an impact on your insurance rates. For instance, if you have access to private laneway or garage parking, which presumably many of the residents in these neighbourhoods do, you could pay lower rates because insurance companies view this as safer than street parking, where theft and damage are more likely to occur.

10. M4M: 22.0% less expensive than the city’s average

Neighbourhoods within this postal code: Leslieville, Studio District, Riverside, East Chinatown, Port Lands

This family-friendly area is home to many self-contained neighbourhoods meaning residents don’t have to venture outside their borders to take care of basic everyday needs such as groceries. Most of these neighbourhoods are close to downtown, which means residents maybe don’t drive as much to get around and instead often use transit to get from point A to B.

Port Lands is largely an industrial area with a small residential population which could also be the reason for cheaper premiums in this area.

11. M6R: 22.4% less expensive than the city’s average

Neighbourhoods within this postal code: High Park, Roncesvalles, Parkdale

Neighbourhoods in the M6R postal code include historic Toronto neighbourhoods like Roncesvalles, Parkdale and High Park.

There are multiple transit options in this area, including three streetcar lines that run frequently, as well as a subway stop.

Like the neighbourhoods in the M4W postal code, drivers in these affluent areas can likely afford to absorb the cost of small claims. Generally speaking, when you make a claim with your insurance company, your premium may increase. The less history of claims in your area, the less you’ll likely have to pay in insurance premiums.

12. M6G: 23.1% less expensive than the city’s average

Neighbourhoods within this postal code: Seaton Village, Palmerston-Little Italy, Koreatown, Bickford Park, Bracondale Hill, Hillcrest Village, Davenport

The neighbourhoods in the M6G area are home to some of the cheapest premiums in town. The neighbourhoods in this area run along Bloor Street West and Dufferin and are well-served by public transit.

This could be contributing to lower premiums, as well as the fact that while many might have vehicles, they may use transit more frequently than they drive.

13. M4N: 23.5% less expensive than the city’s average

Neighbourhoods within this postal code: Lawrence Park, Wanless Park, Yonge and Lawrence, Teddington Park, Sherwood Park

Conveniently located along Yonge Street, the neighbourhoods in this postal code benefit from the cheapest auto insurance in Toronto. This area, commonly known as Uptown, is a quieter residential area with presumably fewer collisions and theft compared to other busier neighbourhoods in the city. It's also close enough to downtown to take transit.

Methodology

- Applicant's age: 30-39

- Clean driving record (i.e. no past policy cancellations; no accidents; no licence suspensions; no traffic tickets)

- One (1) driver and one (1) vehicle on auto insurance policy

Save 20% on average on car insurance

Compare quotes from 50+ Canadian providers in 3 minutes.

About the authors

Zandile is a freelance personal finance journalist. She previously worked as a personal finance writer at LowestRates.ca and before that, the content editor for Real Estate Management Industry News. As a self-proclaimed budget warrior, Zandile dedicates most of her time to advocating for financial wellness.

Lisa is a senior editor in the personal finance space. Her work has appeared in Reader’s Digest, Toronto Life, Canadian Living and TVO. As a child, she diligently hoarded the $50 bills that fell out of her Christmas cards. Adult Lisa is working hard to resurrect those stockpiling tendencies.

Comments