Housing affordability has never been this bad in Toronto, says RBC

By: John Shmuel on September 29, 2017

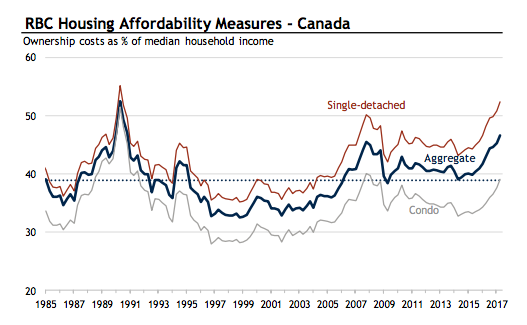

The Royal Bank of Canada has released its quarterly housing affordability report and has found that Canadians’ ability to afford a home has deteriorated to a level not seen since the housing bubble of the late eighties.

RBC’s index shows that homeowners in Canada, on average, now require 46.7% of their income to service a mortgage. Specifically, the report looks at the proportion of median pre-tax household income that would be required to service the cost of mortgage payments across 14 different cities in the country.

Certain cities, however, are skewing the national average substantially.

In Toronto, the housing affordability measure “skyrocketed” to 75.4%, meaning the average earner would require three-fourths of their annual income to go toward servicing a mortgage in that city.

“The Toronto area experienced the biggest deterioration among the local markets tracked by RBC,” the report said. “RBC’s measure has never been this poor in Toronto.”

While Toronto’s affordability has been deteriorating the quickest, it’s Vancouver that still takes the unaffordability crown. The measure in that city rose to 80.7% in the second quarter of 2017, following two straight quarters of improving affordability. That means that Vancouver is now 22 basis points above its long-term affordability measure of 58.2.

RBC also singled out Victoria as another market with rapidly deteriorating affordability. The city has seen prices for housing rise quite quickly in the past year — much of that being blamed on cooling measures implemented in Vancouver.

“Policymakers will want to monitor developments in Victoria closely as well,” RBC said in its report. “Housing affordability pressures in that market have intensified steadily in the past year. Victoria, in fact, has seen the second-largest decrease in affordability since the second quarter of 2016 after the Toronto area. Events in Vancouver’s market—including the introduction of the foreign-buyer tax—contributed significantly to fuel property values in Victoria.”

Outside of Ontario and B.C., however, the picture for affordability looks much more stable. Take a look at affordability in the 12 other major cities RBC tracks.

Calgary: 39.2

Edmonton: 30.3

Saskatoon: 32.1

Regina: 28.7

Winnipeg: 30.7

Ottawa: 37.3

Montreal: 41.5

Quebec City: 34

Saint John: 24.5

Halifax: 32.1

St. John’s: 27.7

As you can see, there are still a few cities in Canada that allow you to spend less than one-third of your income on servicing a mortgage. Some cities — such as Montreal and Saint John — are actually below their 30-year affordability average.

RBC also has a warning for those thinking about buying in Toronto or Vancouver. It believes that interest rates are going to rise faster and sooner than many are currently anticipating.

“The days of ultra-low interest rates in Canada are over,” RBC says in its report. “Back-to-back increases in the overnight rate by the Bank of Canada in June and September made it clear.”

Higher interest rates are expected to erode affordability even further. For instance, for every one percentage point increase in interest rates, it’s expected that affordability will erode by 3.5 percentage points.

That’s significant, because by the end of 2018, RBC predicts that the Bank of Canada will raise its benchmark interest rate by one percentage points in total, bringing the rate to 2%.

Use our comparison tool to see the lowest mortgage rates from leading Canadian banks and brokers.

Compare rates432e.jpg)

b188.jpg)